Open in Claude

Open in ClaudeThe most telling detail in Digiday's June 2026 report on Google Zero is that Time built a dashboard with a switch to turn Google referral traffic off — and ran the business as if it were already gone. That is not contingency planning. That is a publisher conceding that the open-web traffic deal is ending and pricing the future on something else entirely.

- Google organic search traffic to over 2,500 news sites fell 33% globally and 38% in the US between November 2024 and November 2025, per Chartbeat data in the Reuters Institute's 2026 trends report.

- News executives expect search referrals to drop a further 43% over the next three years, with one in five expecting losses above 75%.

- The publishers moving early are not trying to recover clicks — they are decoupling revenue from pageviews, building direct relationships, and pushing reach onto platforms they don't own.

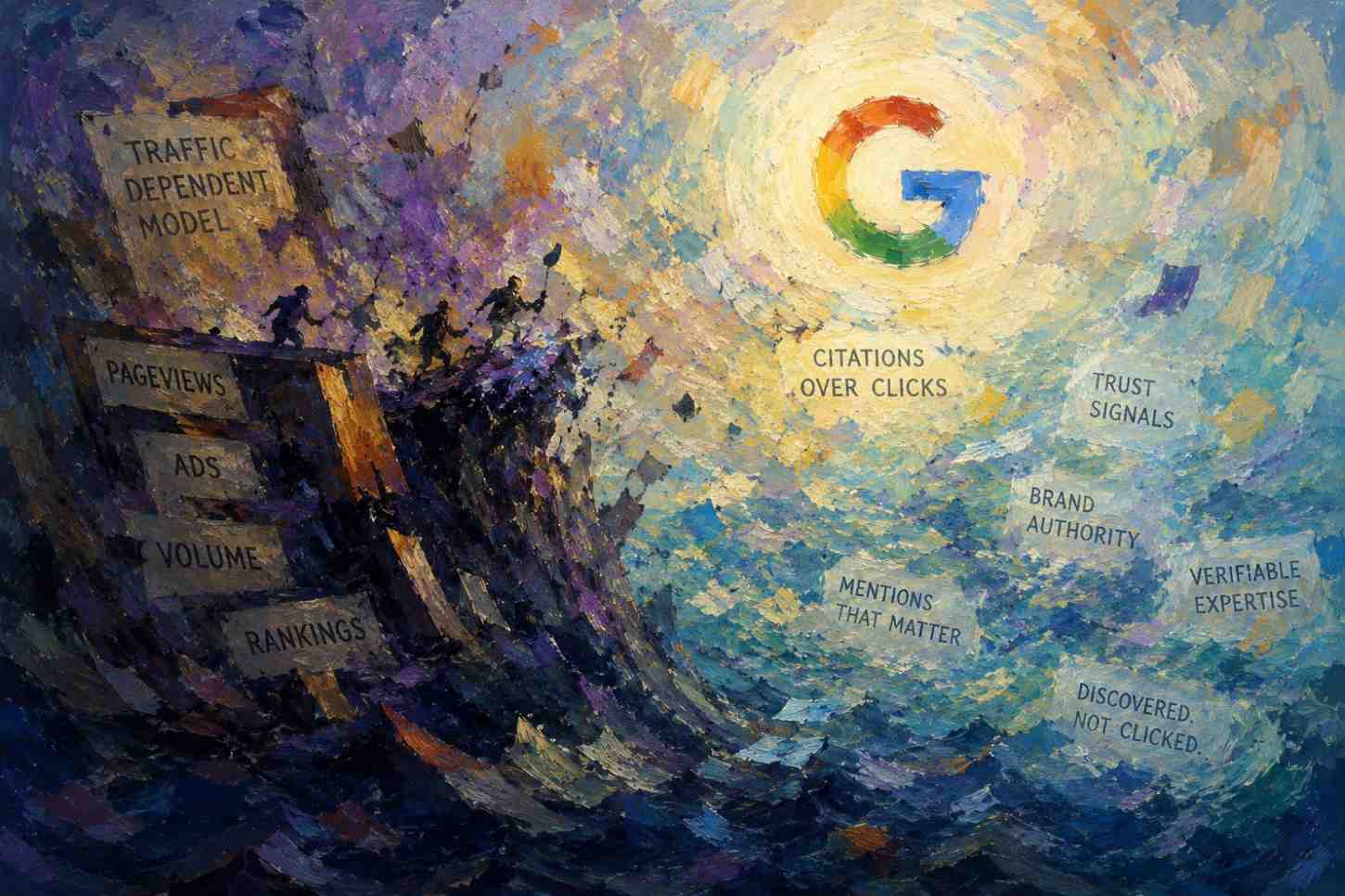

- The mechanic underneath the panic is a shift from a click economy to a citation economy: AI engines still need publisher content to answer, but the click that paid for it no longer arrives.

- Whoever builds the payment rail for citation — not whoever recovers the most traffic — captures the next decade of media economics.

What 'Google Zero' actually describes

Google Zero is the scenario in which Google search stops sending meaningful traffic to publisher sites and becomes a destination that answers the query itself. The threat sharpened after Google's 2026 developer conference, where the company detailed AI-powered changes to search explicitly designed to keep users on the results page.

The point is not whether the number reaches literal zero. It is that the assumption underwriting two decades of digital publishing — that producing content earns a click, and the click earns revenue — no longer holds. The content still gets used. The click is what disappears.

The click economy and the citation economy, side by side

For twenty-five years the open web ran a clean loop: publishers produced content, Google sent traffic, advertisers paid against that traffic, publishers got paid. Attention was rented per click, and the click was the unit everyone settled on.

The agentic web keeps the dependency and breaks the settlement. AI engines extract, synthesize, and cite publisher content to build an answer — but the user stays inside ChatGPT, Gemini, or Google's AI Mode. Influence is allocated per citation; revenue is not. The publisher is more necessary than ever to the answer and less compensated than ever for it. That gap is the defining feature of the citation economy, and nothing in the legacy ad stack closes it.

What Digiday reported, and what the numbers confirm

Digiday spoke to six executives at large publishers in June 2026. Their playbooks diverge but rhyme. Time, per COO Mark Howard, pivoted toward franchises, events, and branded products, dropped its paywall, and watched Google's share of its traffic fall from 60% to 51% while direct traffic rose to roughly 30%; ad revenue grew 22% year over year in 2025. One large lifestyle publisher built a model capping AI Mode at about 80% of searches and forecasts another 30–40% drop in Google referrals. Another reported Google traffic down 60% over two years while the business kept growing.

The macro data backs the anecdote. Chartbeat's figures in the Reuters Institute's Journalism, Media and Technology Trends and Predictions 2026 report show Google organic search traffic to over 2,500 sites down 33% globally and 38% in the US year over year to November 2025, with surveyed executives expecting a further 43% fall over three years. Lifestyle and utility publishers report the steepest declines. The trajectory is not contested; only its speed is.

Why diversifying traffic is necessary but not sufficient

The strongest version of the brand-building case

The smartest publishers in the Digiday piece make a genuinely strong argument: stop chasing scale, build the brand beyond the website, and grow revenue 'unrelated to site impressions.' As one exec put it, plan as if Google goes to zero and anything above zero is upside. Direct traffic, newsletters, events, video on YouTube and Meta, syndication to Apple News — these reduce dependence on any single gatekeeper. It is the right defensive posture, and the publishers running it are growing.

Why off-platform reach without a payment rail still leaks value

But diversification answers the traffic question, not the citation question. When a publisher's reporting is ingested to ground an AI answer and the user never leaves the engine, that publisher has supplied the value and captured none of it — no click, no impression, no subscription prompt, nothing. Building brand equity makes you more likely to be cited. It does nothing to make you paid for the citation. Influence stripped of a revenue mechanism is not a business model; it is a subsidy to the engines doing the citing.

What this means for brands and for publishers

For CMOs, media buyers, and agencies: ringfence the AI-visibility line now

If publishers lose the click, brands lose the blue-link real estate they paid to occupy. The funnel increasingly runs through a synthesized answer the brand cannot bid on through legacy search engine advertising. Treat AI visibility as a discipline distinct from SEO and SEA, with its own budget, owner, and KPIs. Audit how much of your current funnel already depends on AI-surfaced answers, and ringfence a 2026 test budget before a competitor is the one being recommended inside the answer.

For publishers: price the future on citation, not on traffic recovery

Stop modeling toward a traffic rebound that is not coming. The durable position is to be the source of record that AI engines cite — and to get paid for occupying it. That means a citation-based revenue layer: native ad formats served inside AI answers, with the cited publisher in the value chain. Diversified direct revenue keeps the lights on; a payment rail for citation is what turns continued relevance back into a business.

Three signals to watch over the next 18 months

The ad layer the citation economy needs is already forming. OpenAI began testing ads in ChatGPT in February 2026, and Google has told advertisers it will bring ads to Gemini. eMarketer projects US AI-search ad spending rising from roughly $1.1 billion in 2025 toward $26 billion by 2029. Watch three things: whether sponsored placements stay walled off from the answer or get woven into the cited sources, whether AI licensing deals shift from one-off lump sums to usage-based terms, and which player standardizes citation pricing first. Pricing power will sit with whoever sets that benchmark.

Conclusion

Hold on to this: the publishers stress-testing life without Google are right to decouple revenue from pageviews, but traffic diversification only defends the old economy — it does not capture the new one, where their content still powers the answer and the click never arrives. The missing piece is a payment rail for citation. Smalk AI is that rail — an AI Search ad network that places native ads inside AI-generated answers through Generative Engine Advertising (GEA) and opens a citation-based revenue stream for the publishers whose content fuels those answers. What to watch next: which player sets the first pricing benchmark for sponsored citations, because that is the moment the citation economy prices in.